Do Not Honour Decline Code

Do Not Honour (or “Do Not Honor”) decline errors are one of the most common payment failures in e-commerce. This type of error gives no explanation for the reason behind the decline and risks turning a ready-to-buy customer into a lost sale.

Removing roadblocks during the payment process is essential for maintaining customer trust and optimising your business’s sales. Your choice of payment processor is key to avoiding problems that lead to Do Not Honour codes, increased customer churn, and lost revenue.

What Is a Do Not Honour Decline Code?

Do Not Honour is a generic response code issued by the cardholder’s bank that instructs the merchant not to approve the payment. This response is commonly identified as “response code 05.”

Unlike other codes, it doesn’t signify one specific problem. Instead, it acts as a broad signal that the bank has decided that the transaction shouldn’t go through. Issuers sometimes use 05 even when a more specific code exists.

Why Doesn’t the Bank Give a Reason for Do Not Honour Codes?

Banks deliberately keep this response vague for several important reasons:

- To protect fraud detection systems: Providing detailed decline reasons could reveal how anti-fraud systems work. This would make it easier for fraudsters to bypass them.

- To protect cardholder privacy: Some specific instructions could reveal highly sensitive financial or behavioral information about the customer.

- To avoid revealing internal risk rules: Using generic responses prevents banks’ risk models from being reverse-engineered.

However, the generic nature of a Do Not Honour code is frustrating for merchants because it doesn’t provide them with a clear troubleshooting path. Do Not Honour codes also sometimes cause more serious problems for businesses. Customers who can’t complete a payment assume the merchant caused the issue. They easily lose trust in a merchant when payments don’t work for no apparent reason.

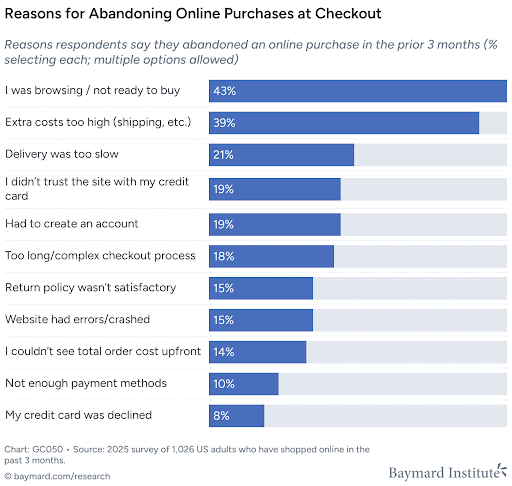

Failed transactions also reduce customer conversion rates because they lead to abandoned purchases and lost sales. According to the Baymard Institute, declined payments accounted for 8 per cent of all abandoned online purchases in a three-month period in 2025.

How Your Payment Infrastructure Helps Reduce Do Not Honour Declines

Modern payment platforms help merchants optimise transaction routing, fraud detection, and credit card authentication. This, in turn, indirectly reduces the causes of cart abandonment and issues that cause loss of trust, like Do Not Honour declines.

Using reliable infrastructure to accept card payments online improves authorisation rates by ensuring transactions are routed through robust security protocols, offering smart routing technology, and accepting a wider range of payment methods.

Work with a payment processor that offers the following features to minimise payment problems both for the customer and your business:

- Access to multiple acquiring banks: A single acquiring bank could experience downtime or decline a transaction due to its particular market strengths or approval criteria. Diversifying allows you to bypass many of these issues.

- Extensive fraud detection tools: Seek PCI-compliance, 3D Secure verification, and an effective fraud scrub for added protection during the payment process.

- Support for global payment methods: Modern e-commerce businesses with a sophisticated global payment gateway offer multiple payment methods and accept a wide range of currencies. This maximises the number of sales your business can make across the world.

Customer reasons for abandoning online purchases at the checkout underline how essential it is to partner with an experienced payment processor. Research into reasons for abandoning online purchases at the checkout revealed motivations like not enough payment methods, website errors, and lack of trust for walking away from a purchase.

Source: https://baymard.com/lists/cart-abandonment-rate

How Card Authorisation Works

It’s important to study how credit card payments are processed to understand where a Do Not Honour decline occurs.

- Customer enters card details: The customer inputs their card information at the checkout.

- Payment gateway sends authorisation request: This is where a reliable payment gateway plays a vital role in speed, security, and routing optimisation.

- Card network forwards request: The transaction is passed through the card network. The most common networks are Visa and Mastercard. The card network then routes it to the correct issuing bank.

- The issuing bank approves or declines: The customer’s bank then decides whether to approve or decline the transaction. It will base this decision on available funds, fraud checks, and authentication requirements.

- Bank returns a response code: The issuing bank sends back an approval or decline alongside a response code like 05 – Do Not Honour.

Do Not Honour declines are generated at the issuing bank level. This means the merchant can’t override it. The payment gateway also can’t force approval. Rather, approval is entirely controlled by the customer’s bank.

Why Do “Do Not Honour” Code Declines Happen?

Do Not Honour declines happen when the issuing bank refuses a transaction based on internal risk checks, insufficient information, or authentication issues.

In Europe, regulations like the EU’s Payment Services Directive (PSD2 and now PSD3) require stronger authentication for online payments to reduce fraud and improve transaction security. Companies without strong anti-fraud tools could suffer more setbacks, like 05 codes at the checkout.

Do Not Honour code declines often happen for one of the following reasons:

- Insufficient Funds or Credit Limit: The issuer may reject the transaction if the cardholder lacks funds or has reached their credit limit.

- Fraud Detection Triggers: Banks analyse transaction behaviour, location, and amount to detect suspicious activity. Any red flags will trigger fraud prevention measures.

- Incorrect Card Details: Incorrect card details typically return specific error codes. However, in some cases, issuers may still respond with a generic Do Not Honour decline.

- Account Restrictions or Frozen Cards: Banks may block cards due to security concerns or account issues.

- Geographic or Cross-Border Restrictions: Some banks block international transactions or certain merchant categories.

Soft vs Hard Declines

Not all declines are the same. Distinguishing between soft declines and hard declines helps merchants decide whether a transaction is worth retrying or should be abandoned altogether.

What Is a Soft Decline?

A soft decline is caused by temporary issues that may be resolved if the merchant retries. These include:

- Insufficient funds in the customer’s account: The transaction should go through after the customer transfers funds into the account or receives their wages (if applicable).

- Network issues that cause technical or communication failures between the merchant, payment gateway, card network, or issuing bank: These could include temporary downtime, timeouts when the bank doesn’t respond promptly, or errors in payment authorisation.

- Temporary bank restrictions: Unusual spending patterns, excessive transactions in a short period, or a first-time purchase with a new merchant can trigger a soft decline.

What Is a Hard Decline?

A hard decline indicates a permanent or high-risk issue during payment. Retrying this type of transaction isn’t recommended as it’s unlikely to succeed.

Permanent blocks that should not be retried include:

- Lost or stolen cards

- Account closure

- Suspected fraud

Should Merchants Retry a Do Not Honour Payment?

Merchants may wish to retry cautiously. However, they should avoid repeated or aggressive retries. This is because it’s impossible to know if a 05 decline is a soft or hard decline.

Retrying a failed transaction sometimes recovers lost revenue, but businesses must handle retries correctly. A generic “try again later” approach is often ineffective without considering timing, routing, and authentication.

Keep the following in mind when retrying a failed transaction:

Timing

Retrying immediately after a decline often results in another failure. This is especially true if the issue is related to temporary risk signals or insufficient funds. Spacing retries improves outcomes.

- Minutes later: useful for transient network or issuer timeouts

- Hours later: allows issuer risk systems to reset or reassess

- Next day: increases success rates for insufficient funds or daily limit issues

Routing

Sending the same transaction through the same acquiring bank will likely produce the same result. Retrying through a different acquirer or payment processor sometimes improves approval rates because issuers may evaluate transactions differently depending on the acquiring route.

Authentication (3D Secure)

If a transaction was declined due to risk concerns, retrying with 3D Secure verification (3DS) often increases the chances of approval. Authentication provides the issuing bank with additional verification and makes the transaction appear more trustworthy.

Please note: Retries sometimes recover revenue. However, excessive or rapid retry attempts could trigger fraud systems and reduce approval rates.

What Should Merchants Do When a Payment Is Declined?

Merchants can’t reverse an issuing bank’s decision to decline a payment. However, they can take some steps to prevent further inconvenience to the customer and reduce involuntary churn and lost revenue.

- Ask the Customer to Contact Their Bank: Only the issuing bank knows the exact reason for the decline. Contacting the bank is the best course of action if the reason for the decline isn’t immediately obvious.

- Offer Alternative Payment Methods: Offering a wide range of payment methods is one of the best ways for e-commerce companies to meet customer expectations. Companies that only offer card payments risk losing out on customers who have embraced types of mobile payments like QR codes or pay by text.

- Try Again Later: Retrying failed transactions at a later time may improve approval rates. However, too many attempts could trigger fraud flags.

Best Practices to Reduce Declined Transactions

Knowing how to act when a payment decline occurs helps merchants complete as many successful transactions as possible. However, taking proactive action to prevent payment declines in the first place is the best way to maintain customer satisfaction.

Make the payment process as smooth as possible by:

Improving Checkout UX

Ensure your checkout is as simple and user-friendly for all your customers. This could include:

- Enabling guest checkout to avoid a lengthy sign-in process

- Only asking for essential information

- Using autofill and address lookup where possible

- Providing clear error messages to help the customer take the next step

Facilitate Smooth Customer Authentication

Customer authentication is a key part of secure payment processing. However, it causes friction if it’s poorly implemented. Prevent false declines by:

- Optimising 3D secure flows

- Avoiding unnecessary authentication triggers

- Utilising an address verification service and CVV where necessary

Support Local Payment Methods

Ensure your payment gateway supports local payment methods to open up your business to cross-border customers.

Recover More Revenue From Declined Payments

Do Not Honour declines are unavoidable in modern payments. However, understanding their ambiguity helps merchants respond more effectively. Although the issuer makes the final decision, the way you handle declines will directly impact recovery and customer experience.

Combining smart retry strategies, strong payment infrastructure, and a seamless checkout helps merchants reduce failed transactions and recover lost revenue. The right approach ensures a Do Not Honour decline doesn’t automatically become a lost sale.

Published: March 9, 2026

Last updated: April 16, 2026

A.J. Almeda is a payment processing and merchant services expert with 15 years of experience helping businesses optimise payment solutions, streamline their checkout process, and improve operational efficiency. With a strong background in e-commerce and digital marketing, he brings a wealth of understanding of online retail, omni-channel sales, and customer acquisition to help businesses grow revenue and scale successfully.